USPS announced a general rate increase (GRI) for both Mailing and Shipping Services that will go into effect on July 14, 2024. The new rates include a 5-cent increase in the price of a First-Class Mail Forever stamp from 68 cents to 73 cents and will raise mailing services product prices by approximately 7.8 percent.

USPS already dominates Residential delivery of 1 Lb. and less packages. However, deeply inducted packages are not moved within USPS’s network. Consolidators have been leveraging long-standing workshare incentives that provide a wholesale rate for the Post Office to deliver the final mile.

Postmaster General Louis DeJoy made it clear that he wants to bring these services in house to help their financial performance.

Here are the “Shipper-focused” highlights:

- Massive loss of ounce-based and DDU induction discounts impacting lightweight e-commerce shipments

- No changes to Priority Mail or Ground Advantage rates

- Matching Nomenclature Standards due to Network Redesign:

- NDC/RPDC (National Distribution Center/Regional Processing Center)

- SCF/LPC (Sectional Center Facility/ Local Processing Center)

- SCF/RPDC (Sectional Center Facility/ Regional Processing Center)

- DDU/SDC (Destination Delivery Unit/Sortation and Delivery Center)

- Elimination of Marketing Samples:

- Will remove the ability to distribute unpackaged product samples in saturation/every door mailing.

- Will need to shift to more expensive shipping options like Ground Advantage.

- Marketing Mail Flats:

- Variable piece price for all weights

- Under 4 ounce will also pay the per pound price

- Updates to “Premium Forwarding Service”

- EVS migration to USPS Ship:

- EVS has been the standard for USPS Manifesting for over 20 years and is scheduled to migrate to “USPS Ship” by Feb. 1, 2025

- Minimum dimensions for Lightweight International “length” increase from 4” to 8.25” and the length plus 2x the diameter requirement increases from 6.75” to 12”. Impacted services include:

- FCPIS (First Class Package International Service)

- CeP (Commercial e-Packet)

- IPA (International Priority Airmail)

- ISAL (International Surface Airlift)

- USPS Returns: Naming changes.

- Will remove the word “service” from the service name

- Will remove plurality (“s”): Returns -> Return

- Postage Platforms migration to USPS API: Currently able to use either the Web Tools/API or 3rd Party Applications. This will sunset that option.

- Payment before processing: Tightening of the rules to allow for abandonment of mail without proof of payment.

- Adding ability to process oversized and dimensionally for “Retail” Ground Advantage. This is something Commercial shippers already enjoy.

- New Zone 10 for off-continent mail and packages.

- Does NOT include Alaska Bypass or LOR

- Includes Priority Mail, Priority Mail Express, and Ground Advantage

- New “Mail.Dat Client”: Need to use the latest version.

- Updates to “Postal One”.

Ground Advantage (Includes renamed: First Class Package Services (FCPS), along with Parcel Select Ground, FC Retail Parcels)

- No Changes (USPS issued a ~5% increase in January)

- Put forth notice of intention to split current Zone 8 off-continent shipments to new Zone 10

- One more distinct USPS usage advantage may be removed

- This one is going to go up against Universal Service Obligations (USO) and may require a rubber stamp from Congress that originally set those standards

Priority Mail (PM)

- No Changes (USPS issued a ~5% increase in January)

- Put forth notice of intention to split current Zone 8 off-continent shipments to new Zone 10

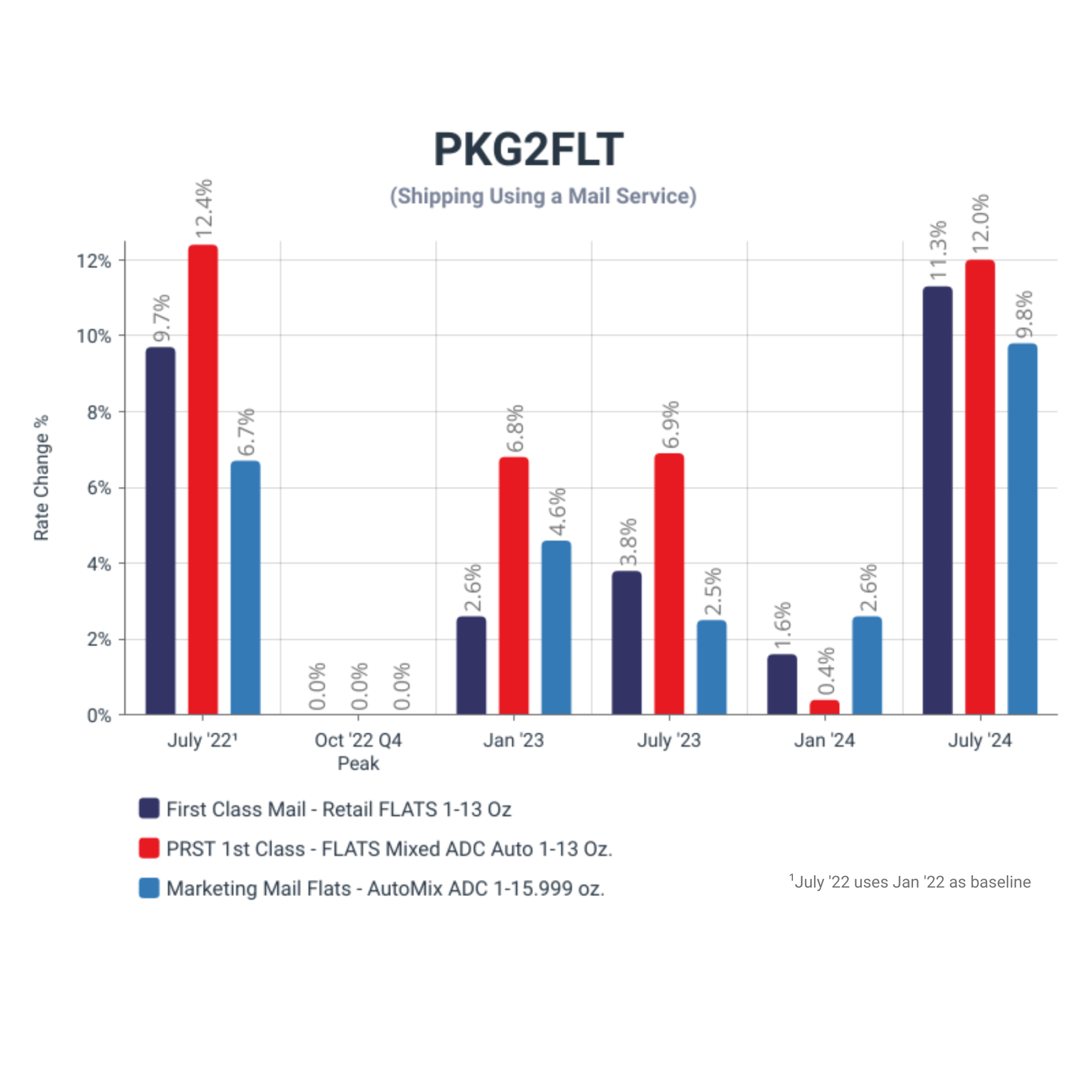

Package to Flat

- Strategy to convert Packages to Flat:

- Produces gross savings of more than 50%

- Items under 5/8” thick with packaging < .75” using customized packaging

- Requires specialized 3rd party tracking (for Client CX) as this is a Mailing service and does not include a final delivery scan

- 3 Rate classes to choose from:

- Retail First Class going up 11.3%

- Presorted First Class Flat going up 12%

- Marketing Mail Flats going up 9.8%

Parcel Select

- This is the massive service category used by Consolidators that use the USPS for the final mile deliveries. Examples include:

- UPS SurePost & Mail Innovations

- DHL eCommerce

- OSM

- Pitney Bowes Newgistics.

- While proposed changes are to the published rates, actual usage and costs of PS programs are controlled via individual vendor contracts.

- These contracts provide relief on the implementation of new rates to the contract’s anniversary date.

- Therefore, the impact of the proposed changes will not take full effect in the first year.

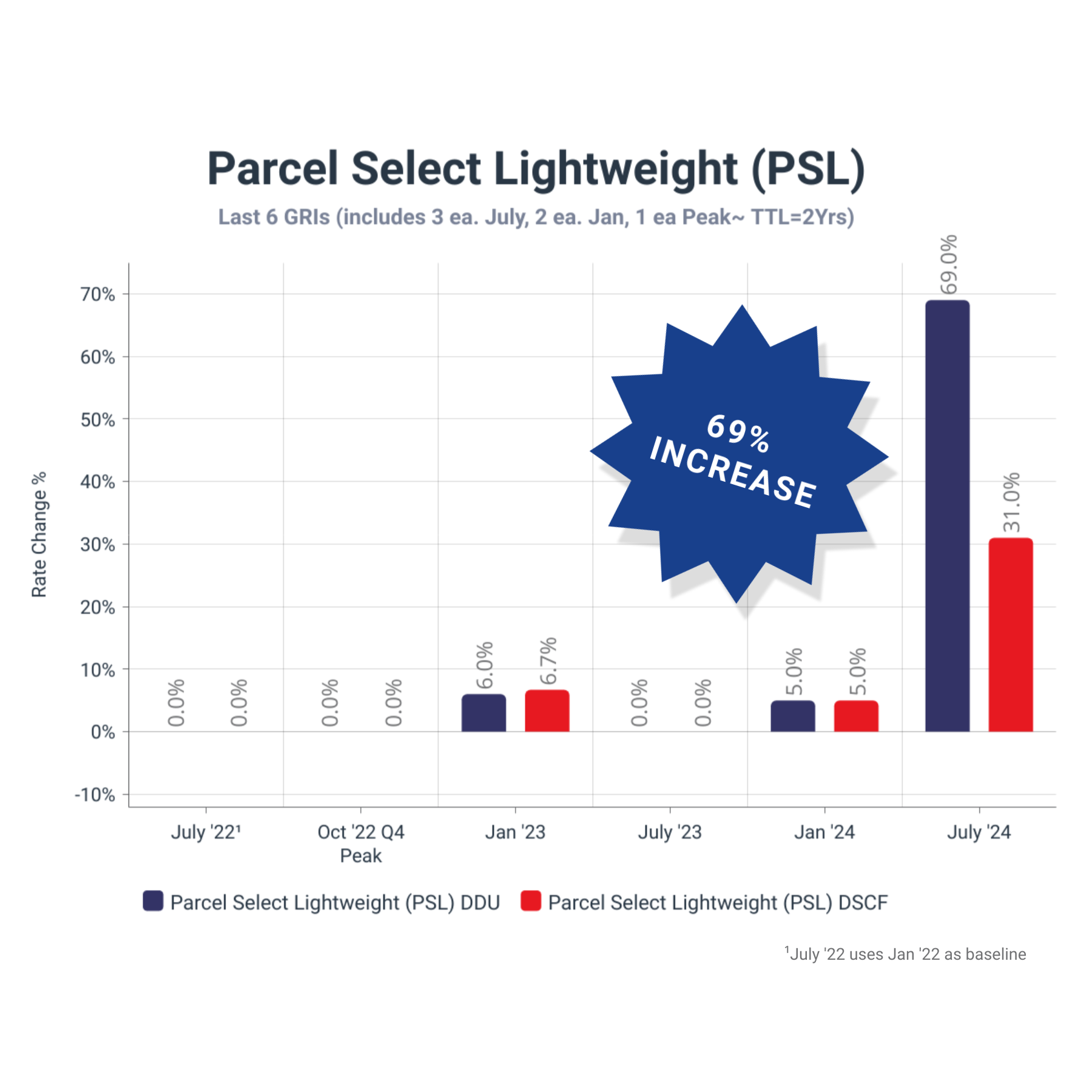

- Up to 69% increase for DDU induction and ounce-based shipments under 13 oz

- The 13-15.999-ounce category is being eliminated, with those packages now rolling up to a full 1-pound rate.

- Ounce-based packages inducted at SCF-level will see a 31% increase and a 49% increase at NDC-level

- DDU inducted parcels above 11 Lbs. will take a 72% increase!

- SCF induction – 1-5 Lbs. pricing going down 4%

- Change to the margin incentive for Consolidators from 33.1% to only 8.6% savings, moving volume from a SCF to DDU induction. (1-5 Lbs.)

- Consolidator use of DDU induction going forward will be for faster service reasons and not for cost savings

So, what does this all mean?

I have closely followed the USPS for the last 42 years.

There has not been this much chaos in the Postal world since the 2007 implementation of the Postal Accountability and Enhancement Act (PAEA) that split the USPS into market dominant and competitive divisions.

Before this change, pricing was based on weight and shifted to “shape-based pricing,” causing a 50% increase in Flats and over 100% increase in the cost to ship a package. Today, the proposed changes will cause price increases of up to 72% for consolidators, and ultimately, consumers will pay more.

How will this affect you as a consumer or as a shipper?

Is that it?

No, there is much more chaos in play.

USPS performance has suffered due to network realignment under the “Delivering for America” (DFA) plan. Last week, Congressional pressure caused PMG DeJoy to pause further implementation until Jan 2025.

On May 23, 2024, high ranking members of the House Oversight Committee asked the Postal Regulatory Commission (PRC) to block the approval of the July ’24 rate change proposal. The focus is on excessive rate increases on the Market Dominant “Mailing Services”, but the bigger (July ’24 GRI) issue is the radical changes to the wholesale “Parcel Select” service.

Let’s dive into the potential winners and losers of this proposed change.

Follow the money

PMG DeJoy wants to control the Parcel Select e-Commerce segment and the profits it generates. By reducing most of the incentives to induct at the local post office, it will drive volume to national hubs at a more expensive rate.

Can the USPS handle the additional network volume?

Conceptually yes, they can do it. They have demonstrated high-performance capabilities during previous peak periods. However, that was an “all hands on deck” time for a limited and expected timeframe.

Currently, the USPS’s on-time performance has dropped to all-time lows, hence the pause in the “Delivering for America” (DFA) plan, and specifically the Mail Processing Facility Rationalization (MPFR), until next year.

Timing of changes and variability by carrier.

Analyzing the USPS projection of only a 2% volume loss against a reported 25% rate increase raises big questions:

- We know USPS pricing is highly “elastic,” meaning there is a very direct relationship between raising prices and a corresponding drop in volume.

- USPS is projecting only a 2% volume loss with 1.5% revenue increase.

- This is due to the timing of the impacted carrier “Negotiated Service Agreement” (NSA) that contains rate increase protections that should cause the new rates to take effect on the contract anniversary date and not in July. Since their projected volume loss is so low, we think most carriers will not have to take the increase until sometime in 2025.

Will the Postal Regulatory Commission (PRC) approve this rate change?

Normally, these are very well-researched and supported changes.

But this one is a head-scratcher.

We simply can’t see the math or how the USPS intends to roll it out. So far, the industry feedback is unsettling. The USPS sent letters to all NSA parties impacted and told them to begin and complete negotiations within 45 days.

We have heard rumors that USPS is playing hardball with some and offering platitudes to UPS, Amazon, and others that they will continue to enjoy low DDU injection rates and maintain ounce-based discounts.

“Wait, what?”

I hope what I have heard is a dirty rumor.

But there is a very real threat that the USPS may pick winners and losers in the marketplace.

This is not their role; as a quasi-Government agency, they must be transparent and fair. America deserves to maintain a Postal system that is fair to all, yet if these changes go through it will dramatically alter the parcel delivery landscape.

How will these changes impact various segments?

Impact on Shippers: Loss of shipping competition and choice would likely drive costs up for shippers (and consumers).

Impact on Consolidators: Consolidators use the existing workshare incentives in different ways. Some have virtually no assets and use PMOD (Priority Mail Open and Distribute) to drop-ship bags of packages to DDUs (Destination Delivery Units/local PO) for final mile delivery. Others have invested heavily in buildings, trucks and people to pick up, sort and transport.

This plan would hurt the companies that invested the most.

Impact on Brick-and-Mortar businesses: This is great news for B&M. This movement to eliminate low-cost transportation for lightweight e-commerce goods will have profound impacts on e-comm. The higher transportation costs will tilt the balance back to B&M while slowing or reversing gains in eCommerce adaptation and use.

FedEx is in a very good position to thrive as it has already transitioned its SmartPost volume in-house and delivers as Ground Economy today.

UPS Mail Innovations is well positioned to pivot. UPS SurePost would likely continue sharing volume with USPS as it benefits them both ways. Added USPS Priority Mail volume will be welcomed as they begin processing USPS volume formerly transported by FedEx.

DHLeC has invested in its own transportation. Its clients benefit from avoiding impacted S&DCs as the majority are transported to the DDUs. It’s big enough that it may go all in and compete by bringing in independent DSPs (Delivery Service Providers) or hooking up with one of the other large players. Could we see the return of the yellow DHL Trucks?

Amazon is the entity that may benefit the most, even though some sales will be lost to B&M. It has already made great strides to deliver volume itself. Should USPS increase costs for SFP (Seller Fulfilled Prime) it will make it easier for Amazon to compete for this volume and also pick up non-Amazon volume. Amazon already is committed to the world’s largest distribution network, and while it will pay more to hand off lightweight packages for remote delivery, it has the choice to keep them in-house. Competitors will find it hard to compete on both price and speed.

Regional Carriers compete well for volume 3 Lbs. and above and would enjoy easier competition with increased USPS pricing.

As a shipper, what should I be doing?

Stay engaged, and let yourself be heard through industry trade groups and your political representatives in Congress. Follow the news on this. While the result may favor one vendor over another, there is no reason to change now, as a lot may change.

Your time will be better spent:

- Flexing your “carrier-mix” power. Expand your ability to evaluate and change carrier programs quickly. Otherwise, it is very hard to negotiate for alternative solutions when your incumbent carrier knows what you face to make a change.

- Apply the service level pricing changes to your distribution summary to gauge the impact of the proposed changes.

- Consider reaching out to third-party consultants who can help you find the right mix and help you negotiate the most favorable rates.

We wish you great shipping success!