Written By Gordon Glazer Senior Consultant, USPS Specialist, Shipware, LLC

USPS announced a general USPS rate increase for shipping services to take effect on January 9, 2022. This year’s changes come on the heels of last year’s massive increases and as the USPS prepares to enter its second Covid-fueled volume peak. Most Shippers will see their costs and postage rate rise 5% to 8% and not the announced average of 3.1%.

Compared to UPS and FedEx announced changes, USPS is going after market share by keeping their price increase lower. Still, any way you slice and dice it, the costs to ship continue to rise. Wondering how your shipping costs are going to change as a result of this? The good news is that many will see very little changes as this general USPS rate increase keeps the essence of the current peak surcharge increase that began in October.

The announced average price change for Priority Mail is 3.1%, however, most shippers will realize a 4.9% increase (1-5 lbs), while ecommerce prices will increase an average of 6-8%. It is noteworthy that certain prices have actually come down. For example, single piece Parcel Select Ground (originally called Parcel Post) significantly decreased pricing by 46% for parcels under 25 Lbs. Therefore, shippers are well advised to study the impacts of these changes on their specific shipping profile.

Here are the “Shipper Focused” highlights:

- Proposed effective date is January 9, 2022

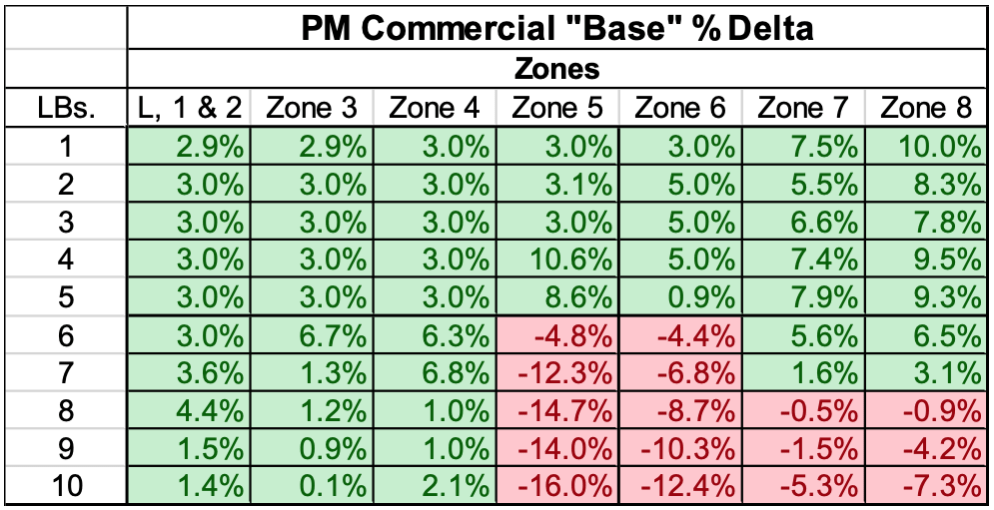

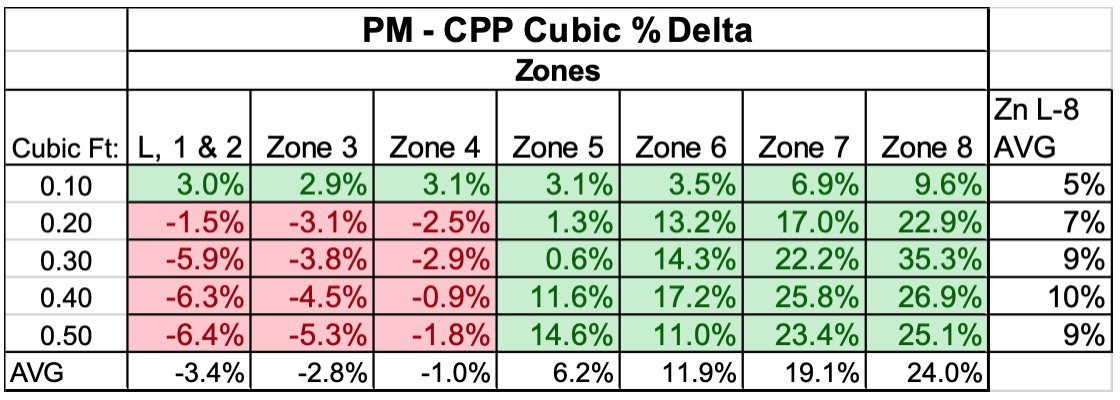

- Priority Mail (PM) 1-5 Lbs. +4.9% (last yr +3%), > 6 Lbs. avg +3.8%, Cubic +7.7% and Regional Flat Rate +4.2%. Flat Rate Envelopes average increase is +5%, Flat Rate average increase for packages + 1.7%. On average 1-5 Lb. pricing is the same as current pricing in effect (which includes the current peak surcharges)!

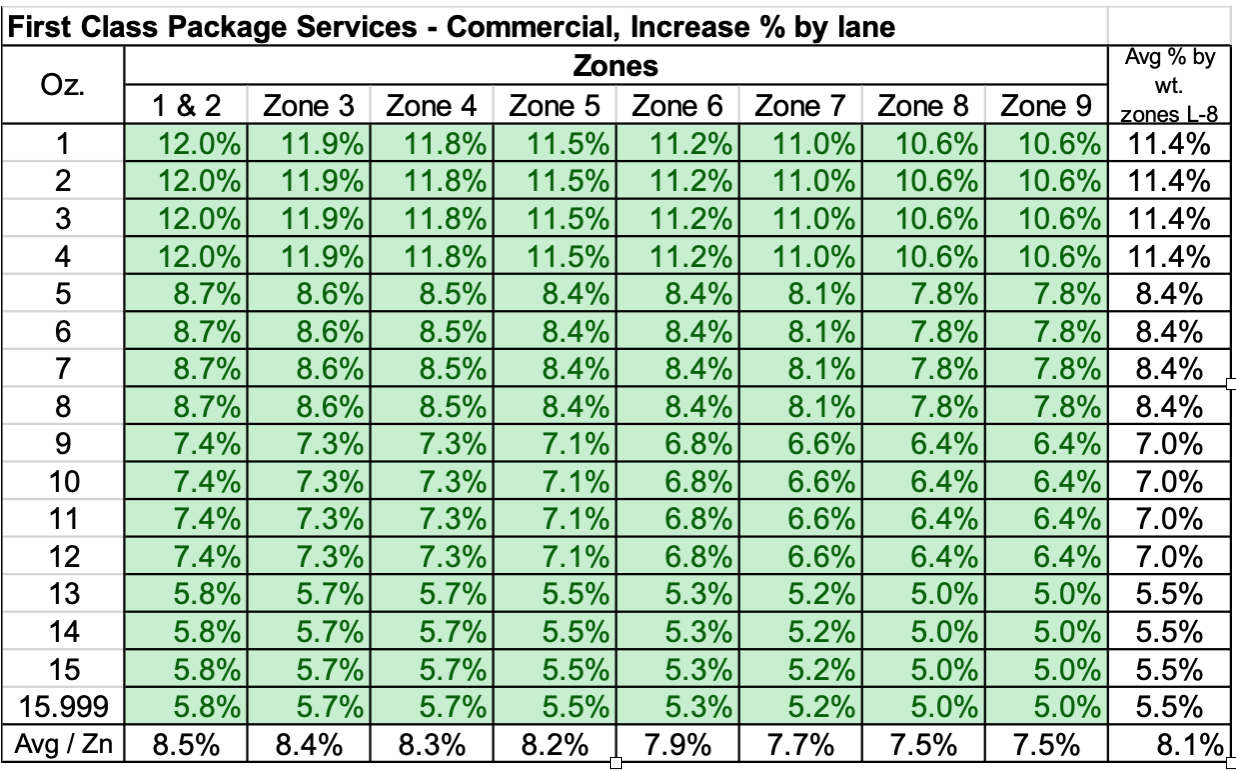

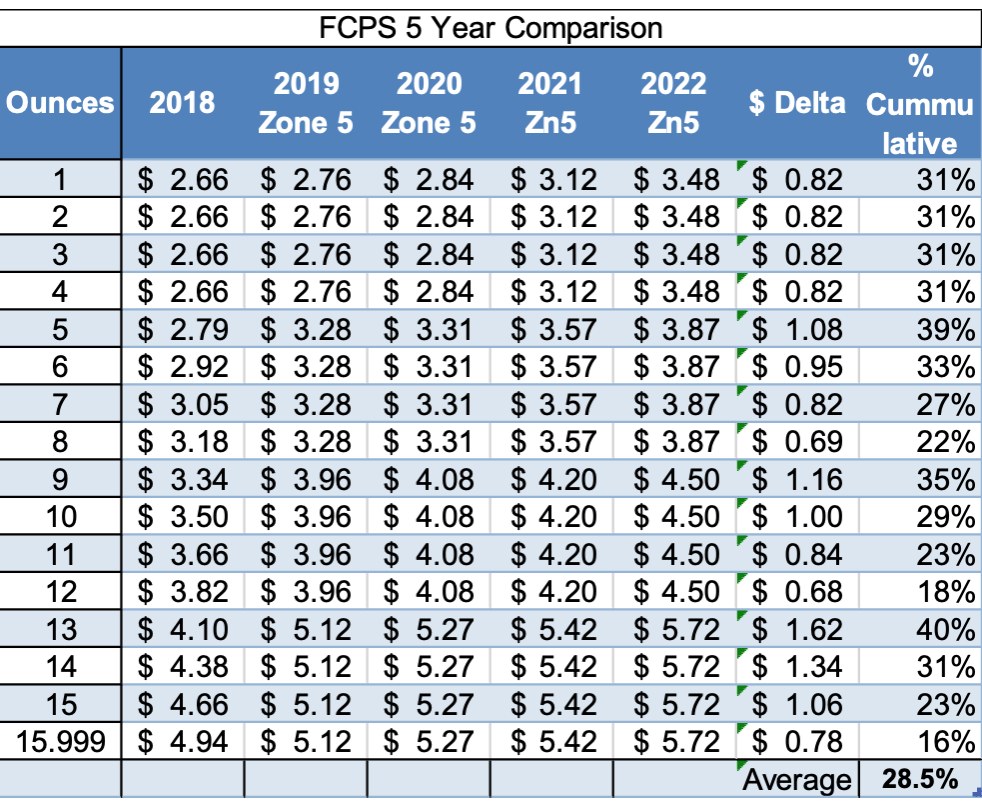

- First Class Package Services (FCPS) +8.1% (last year’s increase was 6%). Historical rolling 5-year cumulative increase(s) creeped up to 28.5% from 25.1% last year. Comparing the new pricing to the October 2021 Peak we see it is virtually identical with only 1-4 ounces receiving a +1.8% increase.

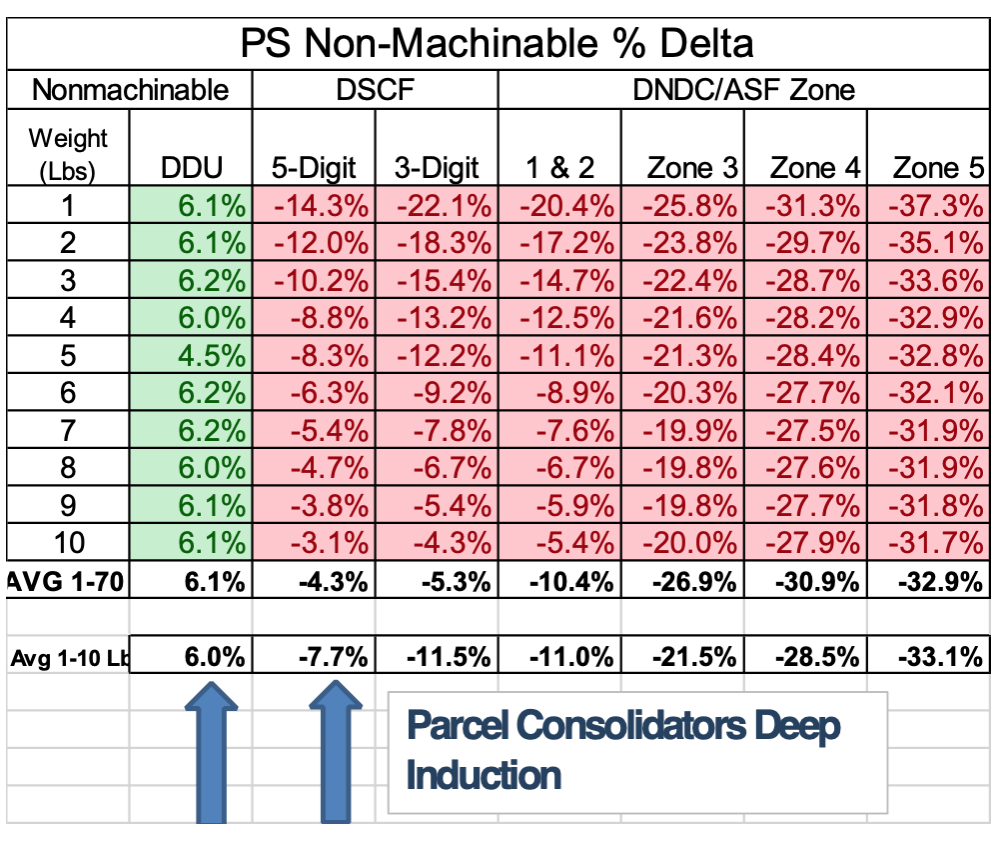

- Economy “Parcel Select” (PS) 1-10 Lbs. increase +6.0% for DDU induction and -7.7% decrease for SCF. The larger Consolidators induct primarily at the DDU level (local Post Office). Therefore, this highly utilized category is essentially the same as the current peak pricing. The next step down in Saturation discounts is called SCF (Sectional Center Facility) and these rates decreased -7.7% continuing a trend as last year these costs were reduced -4.3%

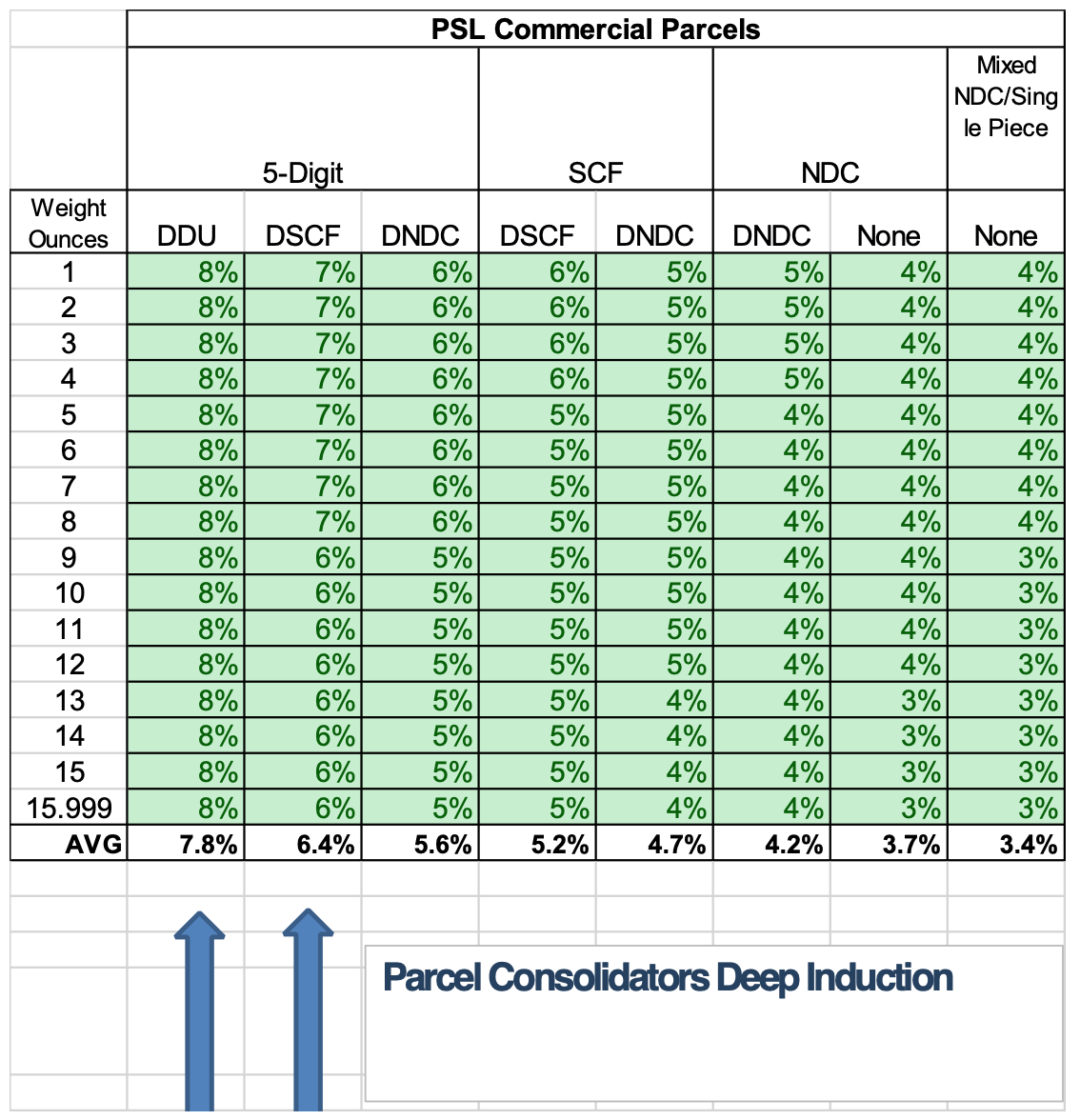

- Economy “Parcel Select Lightweight” (PSL) aka, “less than a pound” +7.8% (DDU induct, SCF + 6.4%) compared to last year’s +18.8%. The DDU proposed rates are the same as current peak, however SCF inducted PSL will pay $1 more per package which is a 36% increase over current peak pricing. Last year’s SCF PSL increase was +19.8% (+6.4% in 2022).

- Parcel Select Ground – Single piece (used for Haz Mat) decreased -46% (1-25 Lbs) and is now -12.8% less than Priority Mail. Last year’s decrease for this category was -4.4%. It appears the USPS is positioning itself to participate in higher weight ground volume.

- Media Mail 1-15 Lbs. increases +11% (single Piece and 5 digit) compared to last year’s decrease of -4.3% (5 digit presort) Note: Single piece increased +2.6% last year.

- Parcel Return Service (PRS) increases are around 5% except Non-Machinable RSCF is only going up +3.2% (1-10Lbs)

- Key Extra Services: Signature Confirmation +8%, Adult Signature +23%

- International Shippers:

- First Class Package International Service (FCPIS) +4% average. UK +6.5%, Australia +6.3%, Germany and France +10%

- Priority Mail International +3.9%

2021 USPS Industry Highlights

- The election-by-mail drama from last year is mostly in our rear-view mirror.

- Like last year, all the national carriers, consolidators, and regionals put limits on, canceled, or restricted volume going into the final part of this year. The USPS, which has no ability to restrict volumes due to the Universal Services mandate, did increase the peak surcharge and is extending the fee for three months this year vs. only one last year. In addition, the Postal Service began early this year to secure space, equipment, and personnel to meet the peak holiday season package and mail delivery surge.

- USPS pricing is highly elastic, which means there is a direct relationship (decrease) in volume as prices increase. In addition, consumers have been well warned of the need to shop early this year due to supply chain shortages and transportation constraints. Brick and mortar operations will likely pull back volume. For these reasons, we believe that “Full Network” USPS (PM, PME and FCPS) is expected to perform significantly better than last year.

- New players: We are currently tracking over a dozen new carriers including both Consolidators, digital aggregation (GPO type programs) and Regionals. OnTrac and LaserShip recently announced a merger with the new entity “LaserTrac” covering 75% of the US population.

The following charts demonstrate increases by USPS service category broken down by weight and zones.

First Class Package Services (FCPS)

Priority Mail (PM)

Parcel Select (PS and PSL)

This growing sector is used by the Consolidators to induct their packages (Amazon is also a high volume user of Parcel Select). Most will recognize Parcel Select shippers by their popular brand names like UPS SurePost, UPS Mail Innovations, Pitney Bowes Newgistics, International Bridge, OSM Worldwide and DHL eCommerce. Collectively known as “Consolidators”, these companies perform and enjoy “Workshare Incentives” from the Postal Service for: collection, sortation, transportation and deep induction within the USPS network for final mile delivery.

- Important to realize that Consolidators use these programs differently, with some offering as many as 3 service levels. It is possible to get 2-3-day transit times to compete with FCPS and PM.

- Note: FedEx SmartPost is now called FedEx Ground Economy and is no longer considered a consolidator since they are now delivering almost completely in-network.

Shippers will have it a bit easier this holiday season to “get their packages picked up”, while delivery times will continue to be stretched due to continuing strains in supply chain (staffing, trucks etc). While you are looking at 2022 impacts, it’s also good practice to look for savings by examining routing logic to make sure least-cost-routing includes all accessorial, dimensional and minimum carrier charges. Review carrier contracts, make note when accessorial discounts may expire intra-contract, and make sure you are achieving targeted discounts. Network with industry peers, attend trade shows, and be proactive in continuously improving your carrier contracts. Savvy shippers understand their distribution profile is unique to them and that rate changes impact each differently. We recommend that mailers and shippers analyze future impact of all carrier rate increases to get out in front of the changes and mitigate cost increases by shopping around. Those that have a diverse carrier mix in place will enjoy the flexibility to minimize holiday surcharges and select the best performing carriers to promote timely delivery. Wishing you great shipping success, and as always, feel free to reach out with questions.